Over the last two decades, Amritt’s senior team has conducted on-the-ground hospital visits across India—including tertiary government hospitals and leading private chains in Delhi NCR, Mumbai, Hyderabad, and Chennai—often alongside U.S. and European life sciences and medical device clients evaluating market entry or expansion.

According to Dr. V. S. Chauhan, Chairman and Managing Director of Prakash Hospital in Noida—a fast-growing multi-specialty hospital serving the Delhi NCR—India’s healthcare system is entering a phase of scale-driven efficiency unmatched by most developed markets. The notes below are derived from his analysis of India’s healthcare trajectory.

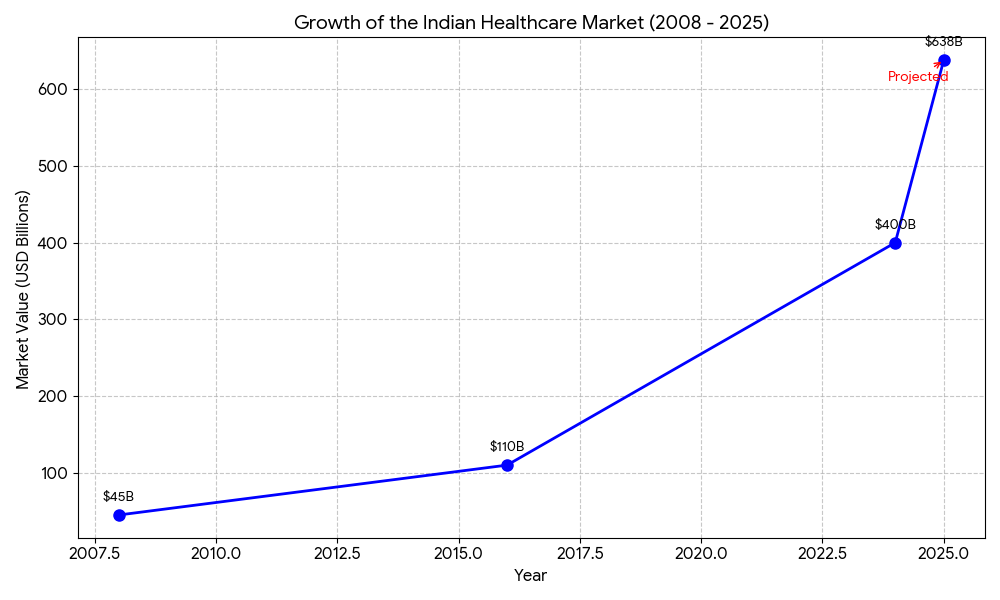

While the Indian healthcare market was valued at approximately $400 billion in 2024, it grew to about $638 billion by the end of 2025, by redefining patient care, financial performance, and investment opportunities.

The Infrastructure and Expansion Dynamic

Currently, India faces a chronic infrastructure deficit with only 1.5 hospital beds per 1,000 people, significantly trailing the global average of 2.9 and the 4 beds per 1,000 seen in nations such as Germany and Japan. To bridge this gap, India needs to add over 1.5 million beds within the next decade. Interestingly, this growth is decentralizing. Following a pattern seen in China during the early 2010s, nearly 60% of new capacity is being developed in Tier-2 and Tier-3 cities. However, unlike China’s state-led model, India’s expansion is fueled by the private sector, which already accounts for over 65% of total hospital capacity.

For device manufacturers and diagnostics companies, this decentralization shifts demand away from flagship metro hospitals toward standardized, volume-driven procurement models—changing both pricing pressure and sales strategy.

Digital Innovation and Data Interoperability

India is overcoming legacy constraints by adopting digital health tools at a pace that rivals or exceeds many middle-income peers. While AI adoption in radiology and pathology still trails the U.S., the integration of electronic medical records and tele-ICU models is accelerating. The National Digital Health Mission serves as a global case study, having created over 500 million digital health IDs. This federated, consent-based digital public infrastructure allows for population-level health analytics — an achievement that remains difficult for many developed nations with fragmented, older systems.

The Cost-Quality Paradox

India’s most compelling differentiator remains its cost efficiency. A cardiac bypass surgery in India typically costs between 10% and 15% of the price of the same procedure in the United States, yet clinical outcomes are increasingly comparable. Despite an annual medical inflation rate of 8% to 10%, India maintains this leadership through frugal innovation and sheer volume. This shift is supported by the rapid expansion of insurance; by 2025, over 550 million Indians will be covered by public or private plans, moving the market away from its historical “out-of-pocket” reliance.

Future Outlook and Challenges

While India produces over 100,000 medical graduates annually—surpassing the combined output of the U.S. and UK — workforce distribution remains a hurdle. The sector is currently adopting international best practices, such as “task shifting” among allied health professionals, to address low nurse-to-bed ratios. As the hospital sector continues to dominate 80% of total healthcare expenditure, the path to a sustainable $200 billion hospital market (projected to reach $194 billion by 2032) depends on balancing this growth with clinical excellence and transparency.